Scenario: A supply has been made and a Tax Invoice has been issued. However, there has been no payment or only partial collection for the debt and it is past a period of 6 months from the date of the invoice. Taxable party could claim back GST paid without write-off the invoice.

What is Bad Debt Relief?

When money that is owed cannot be recovered, it is referred as a bad debt. The money that qualified for bad debt relief needs to be accounted for GST and no payment has been done by debtor after the sixth month from the date of supply.

When do I need to account for Bad Debt Relief?

Bad debt relief can only be claimed when the supply is made by a GST registered person to another GST registered person. It needs to be claimed immediately in the taxable period, after the sixth month from the date of supply.

If the bad debt is not claimed immediately after the sixth month, then the taxable person has to notify the Director General (DG) within 30 days after the expiry of the sixth month on his intention to claim at a later date.

However, it is also required that if collections are made, the repayment of GST is required.

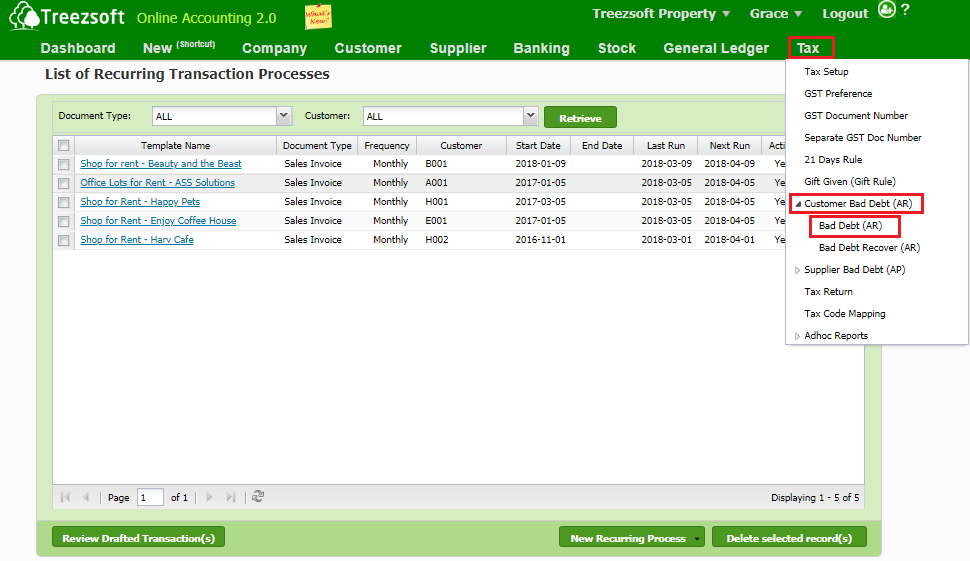

Treezsoft has made it simple for all these processes! To issue Bad Debt Relief, you just need navigate through: Tax > Customer Bad Debt (AR) > Bad Debt (AR).

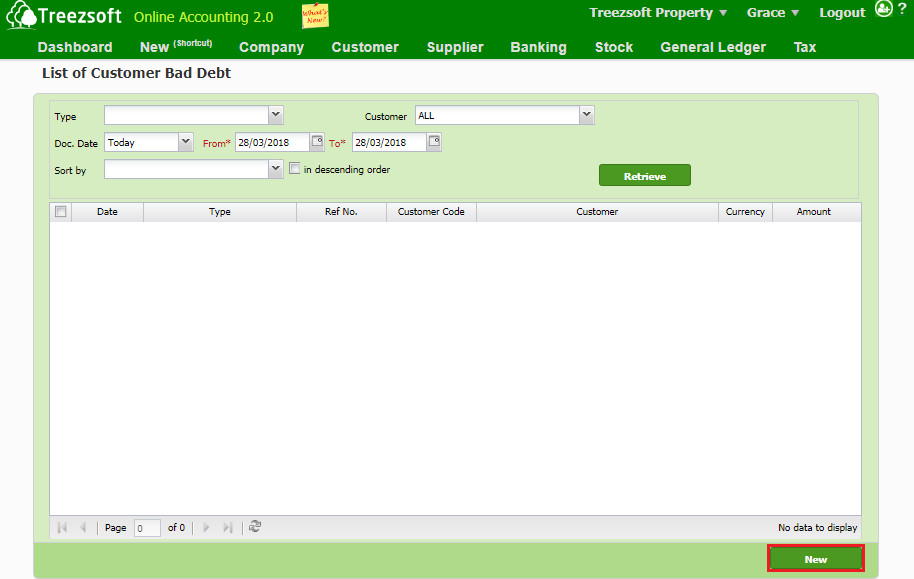

Click on the 'New' button.

Then follow the following steps:

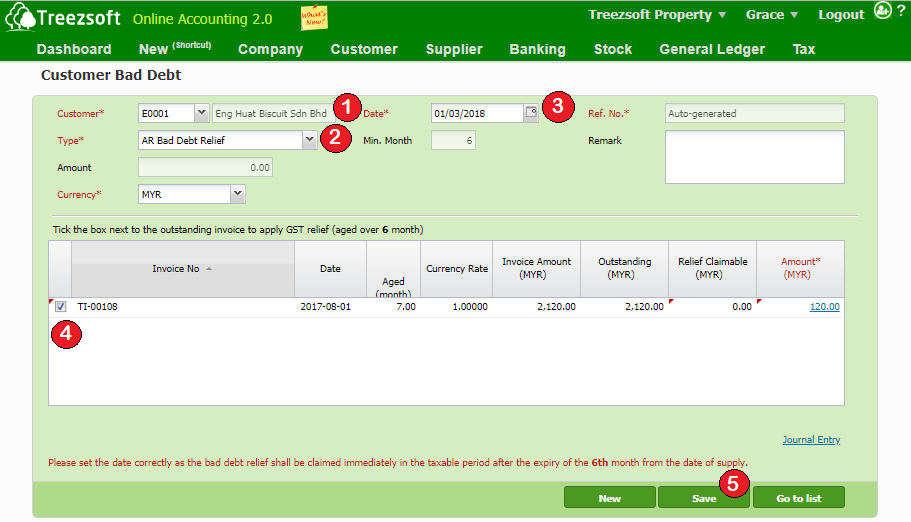

1. Select Customer and fill in the rest of information.

2. Select Type as AR Bad Debt Relief.

3. Select the correct date.

4. Tick on invoice(s) that is to be bad debt relief.

5. Save.

*Please set the date correctly as the bad debt relief should be claimed immediately in the taxable period after 6th month from the date of supply.

Continue reading for GST:

TreezSoft is a cloud accounting software, it allows you to access your financial information anytime, anywhere. It also allows you to create unlimited users for FREE for your account in TreezSoft.

Visit TreezSoft at http://www.treezsoft.com/ to sign up for a 30 days trial account with us!

You can also email us at [email protected] for more enquiries.